Banks press RBI over forex cap

Banks are pressing the Reserve Bank of India to soften a new foreign-exchange rule that dealers say could force the unwinding of large arbitrage positions, deepen trading losses and add fresh strain to the rupee at a fragile moment for the currency market. The central bank has told lenders to keep their net open rupee positions in the onshore deliverable market within $100 million by the end of each business day from April 10, replacing a far more flexible regime under which banks’ boards could set limits linked to capital.The pushback from lenders has grown because the rule change lands after weeks of pressure on the rupee from higher oil prices, foreign portfolio outflows and war-driven risk aversion across global markets. The rupee touched a record low of 94.84 against the US dollar after a sharp slide this week, underscoring the urgency with which the central bank is trying to contain volatility and regain influence over price formation in the domestic market.At the heart of the dispute is a trading structure that banks have used to profit from differences between the onshore market and the offshore non-deliverable forward, or NDF, market. Under the earlier framework, dealers could offset positions across the two venues without breaching broader exposure limits. The new rule narrows that room sharply by capping end-of-day net open rupee exposure in the onshore deliverable market, regardless of how positions are balanced elsewhere. Traders told Reuters that arbitrage books likely to be affected are worth about $10 billion to $18 billion, while Bloomberg reported that banks see total unwinding pressure building toward roughly $30 billion.That distinction matters because the RBI appears to be targeting a channel through which offshore pricing has increasingly spilled back into the domestic market. By tightening end-of-day exposure, the central bank is seeking to reduce the ability of banks to transmit volatility from the NDF market into onshore rupee trading, while making its own intervention in the domestic market more effective. That objective fits with a broader pattern this month, as the RBI has been active in spot, futures and non-deliverable forward markets to steady the currency.Banks, however, argue that the speed of implementation could be costly. Treasury officials have warned that compressing positions before the April 10 deadline may force disorderly exits, widen onshore-offshore spreads and crystallise mark-to-market losses on trades that had previously been profitable. The immediate complaint is not only about tighter oversight but also about the lack of transition time for legacy positions built under the old regime. Reports from the domestic financial press say lenders have asked the central bank to reconsider or provide relief, reflecting concern that a hard cap applied uniformly across banks does not distinguish between speculative bets and market-making activity.The central bank’s tougher line comes as India’s external buffers, while still substantial, have been tested by intervention. RBI data cited in a Reuters report showed foreign-exchange reserves at $709.76 billion as of March 13, enough to cover 11.2 months of imports and about 95 per cent of outstanding external debt. Even so, reserves had fallen notably over the month as the central bank sold dollars to smooth rupee moves. That means policymakers are trying to balance two goals at once: preserving confidence in India’s macro-financial resilience while discouraging trading structures that may amplify pressure during periods of external shock.Another layer of complexity is that the RBI had, only weeks earlier, proposed broader reforms that would ease some foreign-exchange transaction norms for authorised dealers and give market participants greater flexibility in hedging and balance-sheet management. That makes the present clampdown look less like a reversal of liberalisation and more like a targeted response to extraordinary market conditions. For banks, though, the contrast has sharpened frustration: one arm of the regulatory agenda promises flexibility, while another has suddenly imposed a hard operational ceiling on rupee positions.The article Banks press RBI over forex cap appeared first on Arabian Post.

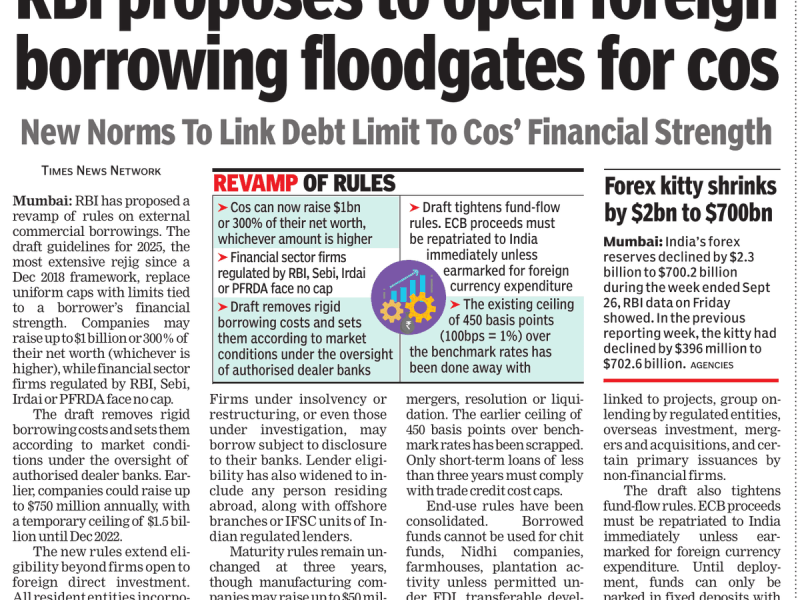

Banks are pressing the Reserve Bank of India to soften a new foreign-exchange rule that dealers say could force the unwinding of large arbitrage positions, deepen trading losses and add fresh strain to the rupee at a fragile moment for the currency market. The central bank has told lenders to keep their net open rupee positions in the onshore deliverable market within $100 million by the end of each business day from April 10, replacing a far more flexible regime under which banks’ boards could set limits linked to capital.

The pushback from lenders has grown because the rule change lands after weeks of pressure on the rupee from higher oil prices, foreign portfolio outflows and war-driven risk aversion across global markets. The rupee touched a record low of 94.84 against the US dollar after a sharp slide this week, underscoring the urgency with which the central bank is trying to contain volatility and regain influence over price formation in the domestic market.

At the heart of the dispute is a trading structure that banks have used to profit from differences between the onshore market and the offshore non-deliverable forward, or NDF, market. Under the earlier framework, dealers could offset positions across the two venues without breaching broader exposure limits. The new rule narrows that room sharply by capping end-of-day net open rupee exposure in the onshore deliverable market, regardless of how positions are balanced elsewhere. Traders told Reuters that arbitrage books likely to be affected are worth about $10 billion to $18 billion, while Bloomberg reported that banks see total unwinding pressure building toward roughly $30 billion.

That distinction matters because the RBI appears to be targeting a channel through which offshore pricing has increasingly spilled back into the domestic market. By tightening end-of-day exposure, the central bank is seeking to reduce the ability of banks to transmit volatility from the NDF market into onshore rupee trading, while making its own intervention in the domestic market more effective. That objective fits with a broader pattern this month, as the RBI has been active in spot, futures and non-deliverable forward markets to steady the currency.

Banks, however, argue that the speed of implementation could be costly. Treasury officials have warned that compressing positions before the April 10 deadline may force disorderly exits, widen onshore-offshore spreads and crystallise mark-to-market losses on trades that had previously been profitable. The immediate complaint is not only about tighter oversight but also about the lack of transition time for legacy positions built under the old regime. Reports from the domestic financial press say lenders have asked the central bank to reconsider or provide relief, reflecting concern that a hard cap applied uniformly across banks does not distinguish between speculative bets and market-making activity.

The central bank’s tougher line comes as India’s external buffers, while still substantial, have been tested by intervention. RBI data cited in a Reuters report showed foreign-exchange reserves at $709.76 billion as of March 13, enough to cover 11.2 months of imports and about 95 per cent of outstanding external debt. Even so, reserves had fallen notably over the month as the central bank sold dollars to smooth rupee moves. That means policymakers are trying to balance two goals at once: preserving confidence in India’s macro-financial resilience while discouraging trading structures that may amplify pressure during periods of external shock.

Another layer of complexity is that the RBI had, only weeks earlier, proposed broader reforms that would ease some foreign-exchange transaction norms for authorised dealers and give market participants greater flexibility in hedging and balance-sheet management. That makes the present clampdown look less like a reversal of liberalisation and more like a targeted response to extraordinary market conditions. For banks, though, the contrast has sharpened frustration: one arm of the regulatory agenda promises flexibility, while another has suddenly imposed a hard operational ceiling on rupee positions.

The article Banks press RBI over forex cap appeared first on Arabian Post.

What's Your Reaction?